Another Example of Traders vs Investors

- emory.sean

- Apr 19

- 4 min read

Big Picture

I think it's clear at this stage that our view that peak uncertainty was likely behind us is playing out. This week added more confirmation.

We remain optimistic, while recognizing that sentiment can still shift quickly. That is part of markets. Staying the course is often the right approach, especially when the backdrop feels most uncomfortable.

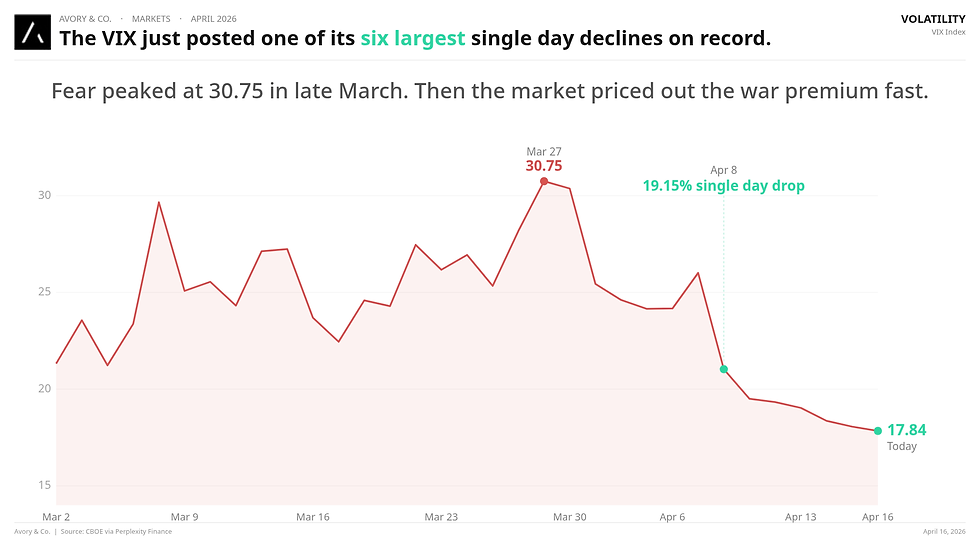

Markets moved higher just as things felt close to their worst. Again that is a good reminder. The VIX is now at 17. Just six weeks ago, it was nearing 31. This was one of the six largest single-day VIX declines on record. That is the market repricing a meaningful risk premium that had been building since February.

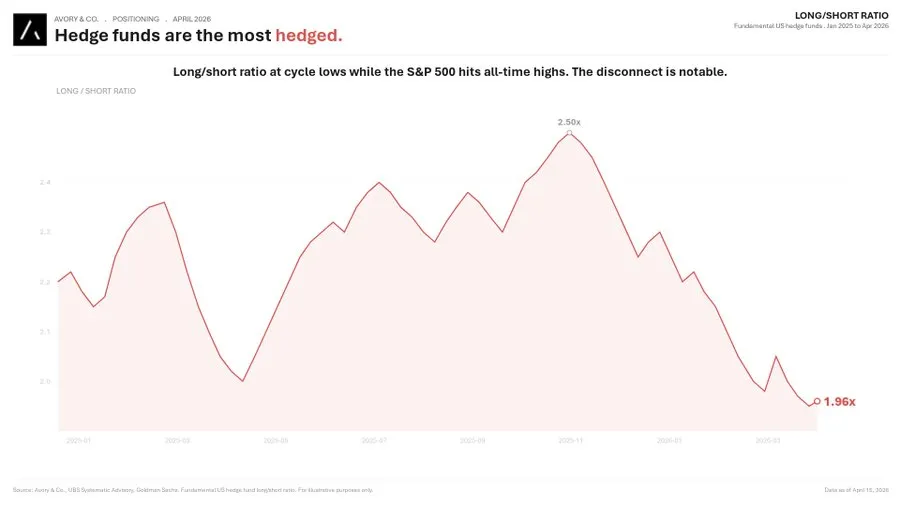

What makes this even more interesting is positioning. Hedge funds remain defensive, with the long/short ratio sitting at 1.96x, a cycle low. In other words, a lot of capital was still positioned for further downside, and the market moved the other way. That kind of disconnect can create real opportunity for patient capital.

Some may ask whether markets now look expensive. That is harder to argue when all-time highs are being accompanied by only 12 companies making new 52-week highs. To us, that likely points to meaningful dispersion beneath the surface.

Simply put, this does not look like a market where everything is expensive and moving together. It looks like a market with selective leadership and plenty of opportunities still out there for investors.

1. The VIX collapsed. One of the six largest single day declines on record.

Fear peaked at 30.75 on March 27. By April 8 it dropped 19.15% in a single session. That is one of six such moves in the VIX's history. Shows again how fast things can change and not to overreact to single headlines.

Today it sits at 17.84. Normal range. The gyrations are not over but the direction seems clearer to us.

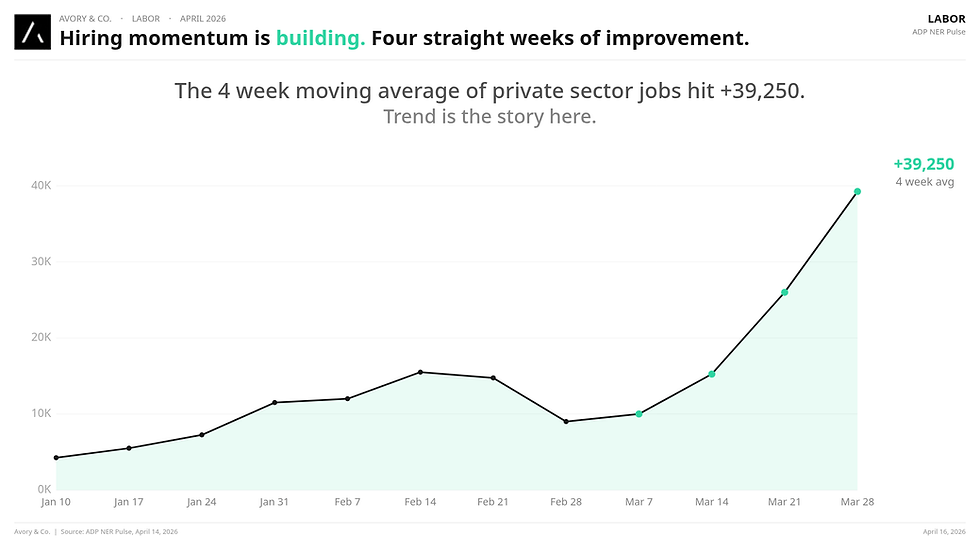

2. Hiring is healing. Four straight weeks of improvement.

The ADP NER Pulse 4 week moving average hit +39,250 private sector jobs added for the week ending March 28. That is the fourth consecutive week of acceleration.

To put this in context, in January that same average was sitting at 4,250. It has nearly 10x'd in 10 weeks. The labor market is quietly getting stronger.

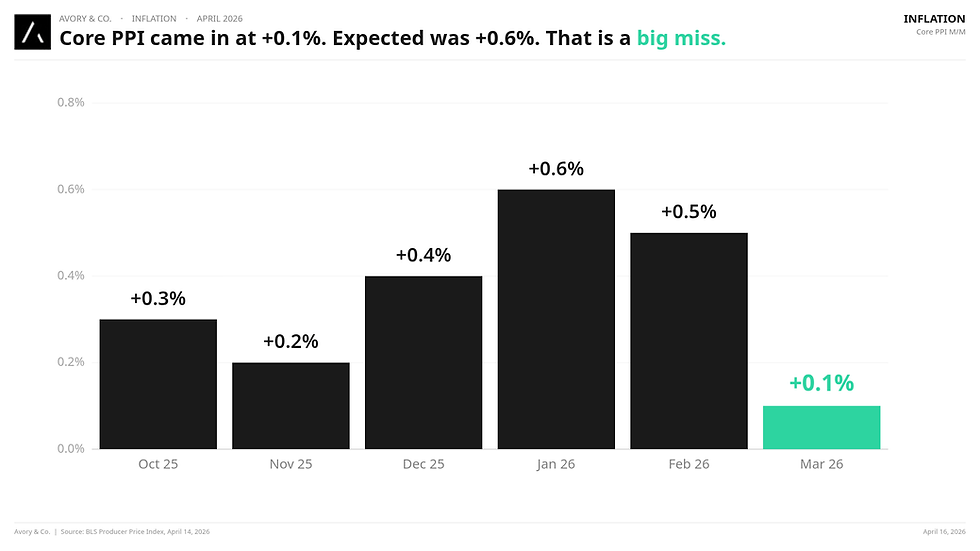

3. Core PPI came in at +0.1%. Expected was +0.6%.

This was a very constructive reading this week. Headline PPI was elevated, obviously energy impacts. But strip that out and core came in at a fraction of the consensus estimate. 0.5% below what was expected and essentially flat.

This is exactly what we have been saying. The inflation story is an energy story right now, not a demand story outstripping supply like 2021. The underlying machinery of the economy is not overheating. That should keep the Fed on the sidelines.

4. The consumer is still spending. Redbook at +7% Y/Y.

Redbook same-store retail sales came in at +7.0% Y/Y for the week ending April 11. That number has been above 6% every single week this year. People keep waiting for the consumer to crack. It is not happening.

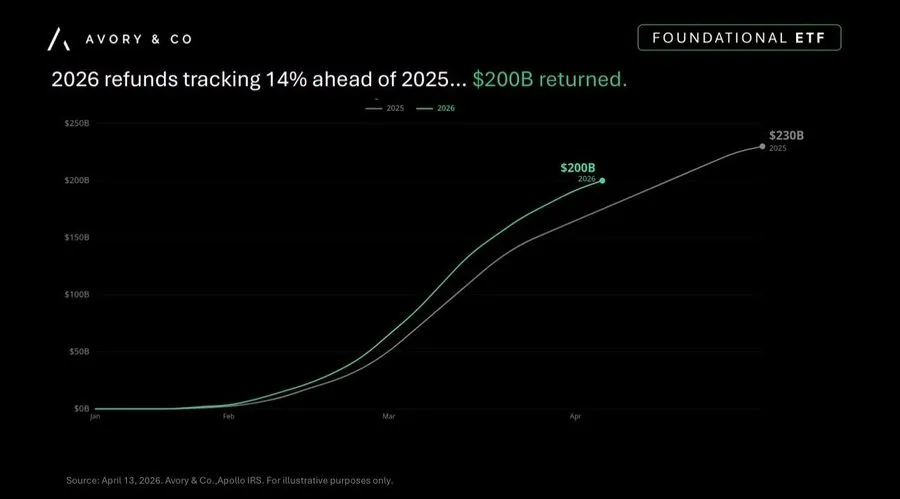

Part of why? Tax refunds. The average refund this season is $3,521 tracking around +14% from last year. About 62.9 million returns processed. That is roughly $200B flowing back into consumer pockets in a compressed window.

5. Tax refunds up 14% Y/Y.

As just mentioned. 14% above 2025. This is good, not bad.

It is not complicated. $200 billion in refunds hits checking accounts right as people were supposed to be pulling back. The consumer keeps spending because the consumer has money.

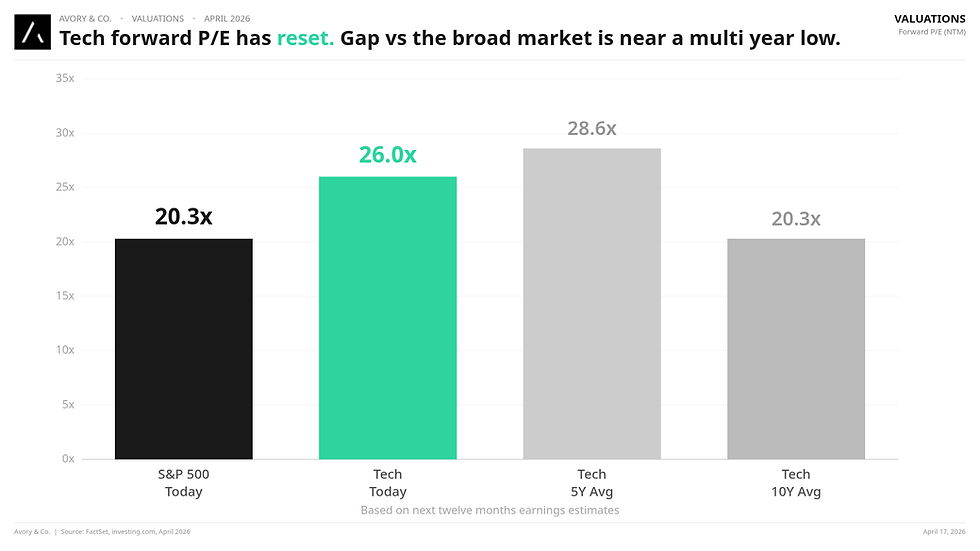

6. Tech valuations have reset.

This one is pretty cool.

Tech (XLK) is trading at a forward P/E of 25-26x today. The S&P 500 broad market is at 20x. That gap is near the smallest it has been in years. It has compressed meaningfully relative to its own history, below on a 5 year average and above on a 10 year.

This is not a call to buy tech blindly. It is a signal that the premium you used to have to pay is less.

7. Market breadth is thin. And that matters.

The S&P hit an all-time high. 12 stocks made new 52-week highs that day. Not normal.

The historical average on an ATH day is 50+. This sub 12 companies has only happened 6 times since 1999. Thin breadth on a new high is not a sell signal, but it is a signal. For us this means more opportunities not less.

8. Hedge funds are at a cycle low in exposure.

Funny. Coming into the week hedge funds were really short. L/S ratio of 1.96x. That is the lowest it has been in years. Funds de-risked hard through the conflict uncertainty and the index ran away from them.

Patient long-term capital owning quality companies through the noise is the structural advantage here. We spoke about this in our last two editions and it keeps playing out.

9. Bank earnings kicked off. The read is constructive.

JPMorgan, Wells Fargo, Citi, and Bank of America all beat this week. All four.

The consistent thread: consumer spending is up, delinquencies are in line, corporate debt levels are healthy, credit quality is stable. JPM was constructive on both sides of the ledger. BofA called out accelerating consumer spend specifically.

Looking Ahead

Earnings season continues. Some of the real signals over the next 3 weeks is whether AI features are actually converting to software revenue.

Conflict resolution. Every week without escalation changes the probability table. Oil futures are the daily tell for us.

Breadth. We want to see more stocks participate in the ATH.

That's all for this week!

About Avory & Co.

Investing Forward.

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn't constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us:

Send us an email:

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube

Channel - Select to view

🎙️ Avory

Podcast - Select to Listen

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.

Comments