12 Charts: We Said It for Years. Finally the Fed Listened.

- Sean D. Emory

- 5 days ago

- 7 min read

Big Picture

💡 Warsh seems to be re-writing the playbook. Real-time data, real rates, real wages. Music to our ears. If you follow our work then you know this!

This was the most important Fed meeting in three and a half years, full stop. Kevin Warsh delivered his first statement at 130 words. Powell's last one ran 341. Yellen's peak was 895. Warsh dropped forward guidance, skipped his own dot, and stood up five task forces on communication, balance sheet, real-time data, productivity, and the inflation framework. That is the Fed moving toward real-time data. We have been beating this drum for years.

We have been on this for 3.5 years now. The lagged-data Fed has been our single biggest critique of this cycle and the source of most of the policy-mistake fear that has whipsawed markets. The way I see it, that fear just got removed. We are not there yet. This was commentary and action is on the way. But when you are a firm focused on the data, the data says things are ok, and markets are on edge due to legacy data, the mental outcome is one of confidence in the future.

Underneath the headlines the data is doing the same thing it has been doing. Real wages are still positive using the real-time inflation data. Retail sales printed +0.9% M/M in May with the control group +0.7%. 5Y breakevens are at 2.31%, below the 10Y at 2.26%, which tells us the market is more worried about a near-term policy error than long-run inflation. Real rates are +1.89%. Restrictive. Anchored.

On the AI side, we are watching open source close in on the frontier in real time. GLM-5.2 hits 74% on agentic coding at max effort against Claude Opus 4.8 at 78%. Token economics at the model layer are not sustainable. Value moves to orchestration. How can enterprises and consumers actually use AI with ease. That is where we are spending time. This has been our view since day one on AI and we think this thesis is starting to show its colors.

And today's headline confirms a thesis we wrote about in March and April when we made our Amazon investment as it fell sharply. Amazon is opening Trainium to outside data centers. Amazon is the king of taking margin out of high-margin, high-capex businesses. Retail, logistics, cloud, and now frontier silicon. That's my view.

[ 1 ] Warsh's first statement ran 130 words. Powell's last one ran 341.

This is what a Fed pivot looks like in literal word count ha. Greenspan's January 2002 statement was 128 words. Yellen peaked at 895 in September 2014. Powell averaged 400 to 500. Warsh came in at 130. He dropped forward guidance entirely. He skipped his own dot. He stood up five task forces. The Committee moves to real-time data, at least that is what he said during a 2 min stretch during his press conference. We have said this for quite some time here at Avory and this is very very very welcomed news.

Here's our post from 2022, just to show how long we have said this! Fed was using legacy data tools, therefore market pricing in policy mistakes.

[ 2 ] Retail continues to defy economists. Matches our view though if you read this weekly!

May retail sales came in at +0.9% M/M versus +0.6% expected. Control group +0.7%. Ex-autos +0.6%. Restaurants and bars +0.8%. The control group feeds directly into GDP and it just printed the strongest read in months. The consumer can keep spending because the consumer is still ahead. Same story, different week. You heard it here first and why we remain confident in our view that you want to own consumer and macro oriented names despite them lagging…

[ 3 ] Real wages remain positive on the real-time cut. They have been all along.

Nominal wages +3.5% Y/Y. CPI-adjusted real wages -0.7% Y/Y because energy is doing damage at the pump. But on real-time basis, our preferred real-time inflation read, real wages are +1.3% Y/Y. The consumer is roughly running behind prices on the headline read and clearly ahead on the real-time cleaner read. This is why spending holds. This is why retail sales were positive, this is why the FED needs to focus on real-time data, and this is why we are happy post FED meeting.

[ 4 ] Real-time inflation today once again ahead of CPI. Real-time data telling a much different story.

Real-time inflation is once again deviating from CPI. That is the gap Warsh just acknowledged. Not the exact number, the idea. The Fed needs real-time data, not lagged surveys. The 30-day real-time read keeps running below CPI which says the official series is still overstating the moment. Funny thing is it has ticked down mostly all year long despite energy surges. This is core reading.

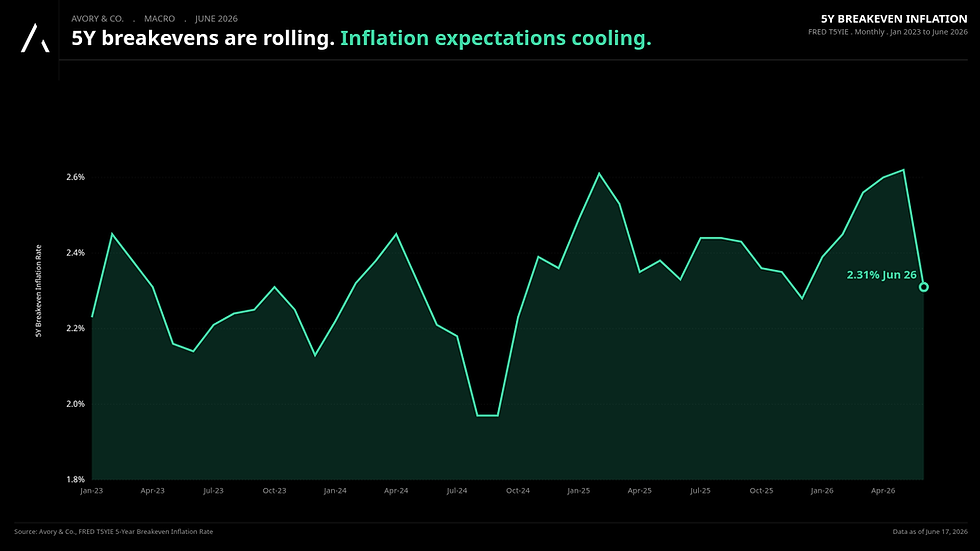

[ 5 ] 5Y breakeven 2.31%. 10Y 2.26%. Market more worried about a Fed mistake than long-term inflation.

5Y breakeven sits at 2.31%. 10Y at 2.26%. The 5Y above the 10Y tells us the market is pricing more risk in the near-term policy path than the long-run inflation outcome. Anchored regime. The 5Y5Y forward at 2.21% is consistent with the Fed's 2% target. The bond market is saying inflation expectations are not the problem. That's the data.

[ 6 ] Real rates are +1.89%. The Fed is still restrictive.

2Y yield 4.20%. 5Y breakeven 2.31%. Real rate +1.89%. That is restrictive. The Fed is still leaning against the cycle and the cycle is absorbing it. This is exactly the setup we have been writing about. Trust the data, not the dots.

[ 7 ] Yields followed oil. Oil is rolling. Yields should follow.

USO at $111.87 and the UST 10Y is at 4.45%. YTD they have moved in near lockstep. Oil leads, yields follow. With Iran tensions easing and the energy curve in backwardation, oil is rolling. The yield should follow. Music to our ears for the long-duration names.

[ 8 ] June dot plot raised the 2026 median to 3.75% from 3.375%. Warsh skipped his own dot.

18 of 19 dots submitted. Warsh abstained. Median 2026 fed funds 3.75%, up from 3.375% in March. 2027 median 3.63%. 2028 median 3.38%. Longer-run 3.13%. Core PCE 2026 revised up to 3.3% from 2.7%. GDP 2026 cut to 2.2% from 2.4%. It is the first meeting and the dots are a forecast not a commitment. Yes hawkish at first glance, but the press conference for us was a little less hawkish and opened the door for flexibility.

[ 9 ] Zoom keeps executing. Top-right of the Frost Radar again.

This week we got the Frost & Sullivan report. They put Zoom at the top-right corner of the 2026 UCaaS Frost Radar. Highest on both Growth and Innovation. Past Microsoft, RingCentral, Cisco on both axes. They keep executing. This is one we own. More to come in another piece.

[ 10 ] Amazon opens Trainium to outside buyers. Confirms our thesis on AMZN.

Amazon is in talks to sell Trainium AI chips directly to outside data centers (Bloomberg). Peter DeSantis confirmed the talks. AMZN +2.55%. MRVL +7.27%. Over $225B in Trainium contracted commitments. Custom silicon at $20B annual run rate, $50B if it stood alone. Trainium 2 sold out, Trainium 3 nearly fully subscribed. Amazon is the king of taking margin out of high-margin, high-capex businesses. Retail, logistics, cloud, and now frontier silicon. This is why we own it.

[ 11 ] Open source is catching the frontier. Fast.

GLM-5.2 hits 74% on agentic coding at max effort. Claude Opus 4.8 sits at 78%. The gap is tiny and the cost curve is collapsing. We are going from expensive closed models to cheap open ones and the token economics at the model layer are not sustainable. The value moves to orchestration. Reinforces our long-standing thesis that frontier will lead and open source is a fast follow.

[ 12 ] Real estate portals like Zillow see little AI search impact. Most traffic is still direct.

GenAI web traffic share. REA 0.48%. Z 0.33%. HEM 0.30%. Some categories are getting reorganized by AI search. Real estate is not one of them yet. Most traffic still arrives direct. Direct means you still control brand, economics, and can drive AI-based outcomes on platform. Worth flagging because the narrative says AI search disrupts everything. The data says it depends and as of right now, not so much.

Net Net

Warsh is the story and the data is the support. The Fed just moved from a backward-looking, forward-guidance-heavy regime to a real-time, data-driven one in a single 130-word statement. We think this removes the policy-mistake fear that has been the biggest risk every cycle, all while underneath the headlines the data confirms our view. Real wages positive, retail sales strong, real-time inflation slower than CPI, breakevens anchored, real rates restrictive at +1.89%, oil rolling, yields should follow. On the AI side the frontier is no longer alone. Today's Amazon news helps solidify the loop on a call we made in March and April. Amazon is the king of taking margin out of high-margin, high-capex businesses, and Trainium is the next chapter. We're staying with the data.

That's all for this week!

Know another investor who'd find this useful? Forward it along or share on your page!

About Avory & Co.

Investing Forward. www.avory.xyz

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn't constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us: Schedule a Brief Zoom Meeting

Send us an email: Team@avoryco.com

Avory YouTube: Channel

Avory Podcast: Listen

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.

Comments