13 Charts: In one year, $416B to +$700B

- Sean D. Emory

- May 1

- 6 min read

BIG PICTURE

💡 Big Tech earnings just confirmed it. Capex is exploding, AI is converting, and the consumer is fine.

Ok so this was the week.

Meta, Microsoft, Google, and Amazon all reported, with Starbucks and Omnicell on the side (holdings). And the takeaway for me is pretty clear: the macro still looks healthier than the CNBC guest circuit suggests.

Across the hyperscalers, demand commentary was strong, AI revenue is converting at scale, and capex commitments into 2026 and 2027 remain massive. Meta raised CY26 capex to $125B-$145B. Alphabet moved to $180B-$190B including Intersect. Microsoft is around $190B. Amazon is still $200B+. That is $700B+ of combined hyperscaler capex this year, off roughly $416B in CY25. +71% Y/Y.

The signal we keep coming back to is simple: these companies are not spending because they hope AI works. They are spending because the demand they see internally requires it.

Susan Li said it well on Meta’s call: “we have continued to underestimate our compute needs.”

I’d say that’s the read from our desk too. Especially platforms like Meta with so much distribution.

And the consumer side still lines up with what we have been discussing. Amazon retail units +15% Y/Y, strongest since COVID. Google Search +19%, with retail and finance strength called out. Not perfect. Not booming everywhere. But still a “good enough” economy.

On AI infrastructure, vertical integration keeps showing up. Amazon with Trainium. Google TPUs generating external hardware revenue. Microsoft Maia 200 live in Iowa and Arizona. Meta rolling out custom silicon with Broadcom alongside AMD and Nvidia.

So yes, we remain constructive. AI is real, the winners are emerging with plenty of time left. Let’s get into it.

[ 1 ] Hyperscaler capex is exploding. ~$710B combined CY26 guide.

Meta raised CY26 capex guide to $125B-$145B (from $115B-$135B). Alphabet bumped to $180B-$190B (from $175B-$185B, now including Intersect). Microsoft committed roughly $190B for CY26 on the call. Amazon held at $200B+. That is ~$710B at the midpoint of guides, all on a capex incl. finance leases basis.

[ 2 ] Amazon AWS +28% Y/Y. Backlog +$120B in one quarter to $364B.

AWS revenue $37.6B, up +28% Y/Y, the fastest growth in 15 quarters. Operating margin 37.7%. Backlog hit $364B excluding the Anthropic deal, up ~+$120B in a single quarter. AI run-rate now >$15B annualized. Bedrock spend +170% Q/Q.

Amazon is on the frontier again.

[ 3 ] Amazon retail units +15% Y/Y. Consumer is fine, full stop.

Worldwide retail units grew +15% Y/Y. Per Jassy, that is "the highest since the tail end of covid lockdowns." North America COMMERCE segment revenue was $104.1B. Advertising revenue $17.2B (+24% Y/Y), TTM ad revenue >$70B.

We care about Amazon retail units specifically because it is the cleanest proxy for actual consumer goods demand. +15% Y/Y is not a weak consumer signal.

[ 4 ] Amazon's chip business. $20B run-rate, $225B+ in commitments.

Amazon disclosed its custom silicon business (chips) runs at >$20B, growing triple digits. >$225B in Trainium revenue commitments. Trainium 2 is sold out, 30% better price-performance vs Nvidia GPUs. Trainium 3 shipping in early 2026, ~30-40% better than T2.

Big tech wants to control the silicon stack and Amazon is moving aggressively. More signal.

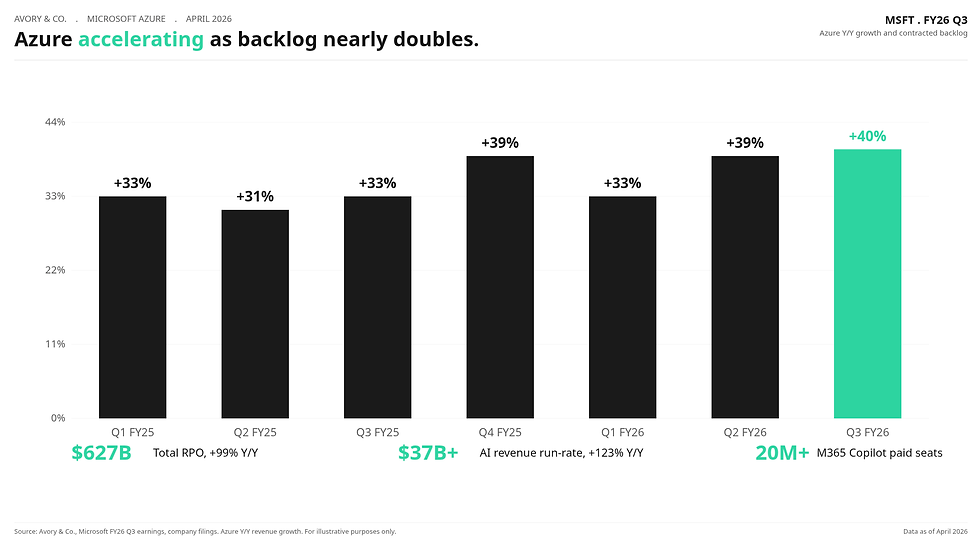

[ 5 ] Microsoft Azure +40% Y/Y. RPO doubled to $627B.

Microsoft crushed. Azure grew +40% Y/Y in FY26 Q3. Total RPO surged +99% Y/Y to $627B. AI revenue now at a $37B+ run-rate, up +123% Y/Y. M365 Copilot has 20M+ paid seats with +250% Y/Y seat adds.

Not sure how I feel about those Copilot seats. As a product I think it's third tier. So Microsoft Azure is doing great, but I still think there is some risk to their productivity suite from AI encroachment.

[ 6 ] LinkedIn +12% Y/Y. Hiring momentum showing up in ads too.

LinkedIn revenue grew +12% Y/Y (+9% constant currency) with growth across all lines of business. Q4 guide is ~+10%.

I always liked to look at this as LinkedIn is a useful real-time read on enterprise hiring and B2B advertiser demand. +12% growth is consistent with the ADP weekly pulse picking up that we flagged in our last edition.

[ 7 ] Google Search +19% Y/Y. AI Overviews are not killing Search.

Google Search revenue $60.4B, up +19% Y/Y. Pichai called out retail and finance verticals driving strength. Search queries hit an all-time high.

This is the cleanest read on advertiser demand and downstream consumer demand. +19% Y/Y growth in Search ads is a strong economy signal.

[ 8 ] Google Cloud +63% Y/Y. Backlog nearly doubled to $462B.

Google also winning in compute needs. Google Cloud segment revenue $20.0B, up +63% Y/Y, with GCP itself growing materially faster than the segment. Operating income $6.6B, tripled Y/Y. Margin jumped to 32.9% from 17.8%. Backlog hit $462B, nearly doubled sequentially, with just over 50% expected to convert within 24 months.

Google is now a real third platform alongside AWS and Azure.

[ 9 ] Meta ad impressions +19%, price +12%. AI working.

Honestly outside of them trying to spend more on things that are working, this was a great quarter.

Meta revenue +33% Y/Y to $56.3B. Ad impressions +19% Y/Y, average price per ad +12%. Both metrics accelerated vs Q4 2025. Reels time spent +10% on Instagram from AI ranking improvements. Facebook video time +8% Q/Q, the largest quarterly gain in 4 years.

Their new Adaptive Ranking Model added +1.6% conversion rate across major Facebook and Instagram surfaces. Value Optimization ARR is now >$20B, more than doubling Y/Y. More than 8M advertisers are now using at least one of Meta's gen AI ad creative tools, up from 4M when first disclosed at Q4 2024 earnings.

This is the AI play.

[ 10 ] Meta business AI. 1M to 10M+ weekly conversations in one quarter.

Meta's business AI weekly conversations grew from ~1M at start of 2026 to more than 10M by end of March. That's 10x in one quarter. WhatsApp ads and Status are scaling, with hundreds of millions of people now viewing them daily.

Zuckerberg framed the strategy directly: "We're building a personal agent focused on helping people achieve the diverse goals in their lives. We're also building a business agent focused on helping entrepreneurs and businesses across the world use our tools and others to grow their efforts, reach new customers, and serve existing customers better. These agents will work together to form an ecosystem."

[ 11 ] Atlassian: AI is a tailwind, not a headwind, for the right software platforms.

We've said for a while that software should not be treated as one bucket. AI is essentially software, and the platforms that integrate it well are going to benefit, not get disrupted. Atlassian's earnings is one of the cleanest data sets we've seen on that thesis.

A few of the standouts. Customers using Rovo (their AI) are growing ARR at ~2x the rate of non-AI customers. AI credit usage is compounding more than +20% month over month. The Service Collection, their AI-heavy offering, is now >$1B ARR growing +30%+ Y/Y. There are other datapoints but clearly software can win.

[ 12 ] Starbucks comps +6.2% global, +7.1% US. Niccol is delivering.

Global comp +6.2%, US comp +7.1%, North America comp +7.1%, China +0.5%.

The strongest in three years and the third consecutive positive print after 7-8 quarters of declines.

Long-time followers know we've been on Brian Niccol for a while. We owned Chipotle when he took over and that worked out. We were patient with Starbucks because it is a different animal but the early returns are paying off.

[ 13 ] Omnicell beat across the board. Titan XT cycle is the next leg.

Omnicell Q1 revenue $309.9M (+15% Y/Y), beat by ~$5M. Non-GAAP EPS $0.55 vs $0.33 consensus, a +66% beat. Non-GAAP EBITDA $44.7M, +42% above estimates. Product revenue +20% Y/Y.

More importantly for our thesis, Titan XT first orders already booked in Q1 2026, with hardware shipments beginning H2 2026 and OmniSphere software rollout in H1 2027. Total replacement opportunity is >$2.5B over the cycle, with bookings ramping through 2026 and revenue scaling in 2027.

Looking Ahead

Jobs data Friday. April NFP and unemployment rate. We want to see continued labor strength but not so hot it changes the inflation read.

Iran. Any news on ceasefire.

Earnings. More earnings next week.

That's all for this week!

About Avory & Co.

Investing Forward.

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn’t constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us:

Schedule a Brief Zoom Meeting

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube": Channel

🎙️ Avory: Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.

Comments