Earnings Beats, AI Focus, and an Infrastructure Shift.

- Avory Team

- Aug 15, 2025

- 3 min read

Updated: Aug 22, 2025

Hey everyone! Happy Friday. More of the same this week as earnings season winds down, with just one company left to report in our portfolio. At the index level, Q2 2025 results are largely in: with 90% of S&P 500 companies having reported, 81% have posted a positive EPS surprise and 81% have delivered a positive revenue surprise. Alongside the beats, “recession” mentions in earnings calls have dropped to multi-year lows.

AI remains top of mind across financial markets, and with jobs holding stable enough and rate projections trending lower, small and mid caps saw a boost, something we’ve been discussing for months. As this continues, we expect more capital to flow toward small and mids, though it won’t be a straight line.

Let’s dig in.

Here is the summary if you want just that:

11.3% debt service ratio.

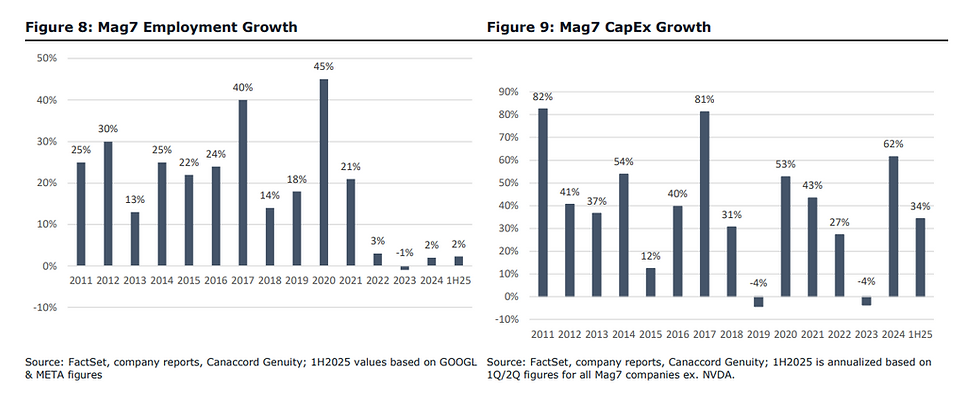

34% CAPEX growth for mag 7.

95% for rate cuts.

Proto $500m opportunity?

So let’s start with what companies are saying. With earning season come closer to an end mentions of “recession” by public companies in earnings calls have dropped to near 0% in aggregate, the lowest in years. This reflects a clear sentiment shift, with fewer executives flagging macro downside risks in their outlooks.

Part of the reason his is because consumer balance sheets remain historically healthy, with debt service ratios as a percentage of personal income still near multi-decade lows. Even in a higher-rate environment, household leverage remains manageable, providing a cushion for continued spending.

Some are also questioning job growth. In the jobs market, big tech hiring growth has slowed, particularly among the Magnificent 7. At the same time, these companies are channeling more investment into infrastructure, accelerating capital expenditure in AI, cloud, and other physical capacity projects over headcount growth. So net net spending is still happening, just priorities have shifted slightly.

Inflation remains a question for some, but not for us. As expected, the July PPI report showed an uptick in the headline reading, driven largely by service inflation. The increase was concentrated in core service categories like healthcare, which are unlikely to be meaningfully influenced by rate changes.

Real-time inflation, as measured by Truflation, continues to show steady and stable pricing in the U.S., currently at 1.9%. It has been a reliable gauge of how inflation actually feels to consumers and how spending patterns compare to the headline data.

Markets are now pricing in a 95% probability of a rate cut in September, with another one and a half cuts expected beyond that. Rate cuts remain the base case for investors heading into the second half of 2025 despite what some would consider a hot PPI.

Now this was an interesting datapoint. For the first time ever, U.S. data center construction is on track to surpass general office construction.

If you look at the chart, office construction spending peaked in the mid-to-late 2010s and held steady for a few years. But since 2022, it’s been in a steep decline, now down roughly 30% from its highs.

Meanwhile, data center construction has been on a straight-line climb. After a modest uptick in the late 2010s, growth really accelerated starting in 2022, with spending nearly quadrupling in just three years. This crossover isn’t just a quirky data point. It’s a reflection of where work and value creation now happens. Productivity is increasingly coming from homes, remote setups, and server racks, not cubicles. AI, cloud, streaming, and digital services all run on these physical backbones, and investors are betting heavily on that infrastructure over traditional office space. Wild.

Speaking of infrastructure, one of our companies, Block, entered the computing infrastructure space with the launch of Proto, a modular high-performance rig designed for Bitcoin mining but also adaptable for AI computing. They held their launch event this week, and we’re looking forward to seeing how this develops in the future. We have nothing embedded in their financials from this, but after this event, the opportunity could be +$500m.

That is it for this week!

About Avory & Co.

Investing where the world is headed.

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn't constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us: Schedule a Brief Zoom Meeting

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube Channel

🎙️ Avory Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.

Comments