Stable Data, Strong AI, and Fed Cuts Ahead.

- Avory Team

- Aug 29, 2025

- 4 min read

Hey everyone! Happy Friday. This was another big week for earnings, not in volume, but in the significance of the companies reporting. Snowflake, Nvidia, CrowdStrike, Box, Nutanix, and Pure Storage all reinforced the same theme: AI spend remains strong. The key development is that spending is starting to migrate above infrastructure into the tools layer, with Box’s launch of its Model Context Protocol (MCP) as a standout and them seeing demand. We saw this last week from Zoom where they saw 4x growth in monthly active users of their Ai product.

On the macro side, economic data was stable enough to keep the Fed on track for cuts, with housing showing cracks, commodities rolling over, and jobs softening but not collapsing.

Let’s dig in.

Here is the summary if you want just that:

Nvidia datacenter revenue: $41B, AI infra spend still massive

Box MCP demand strong, AI spend shifting to tools layer

Housing rents negative Y/Y since June 2023, vacancies 7.1%

Real-time inflation: 2.15%, commodities rolling over

Fed cut odds: 87% Sept, 50/50 Oct, potential 50bps

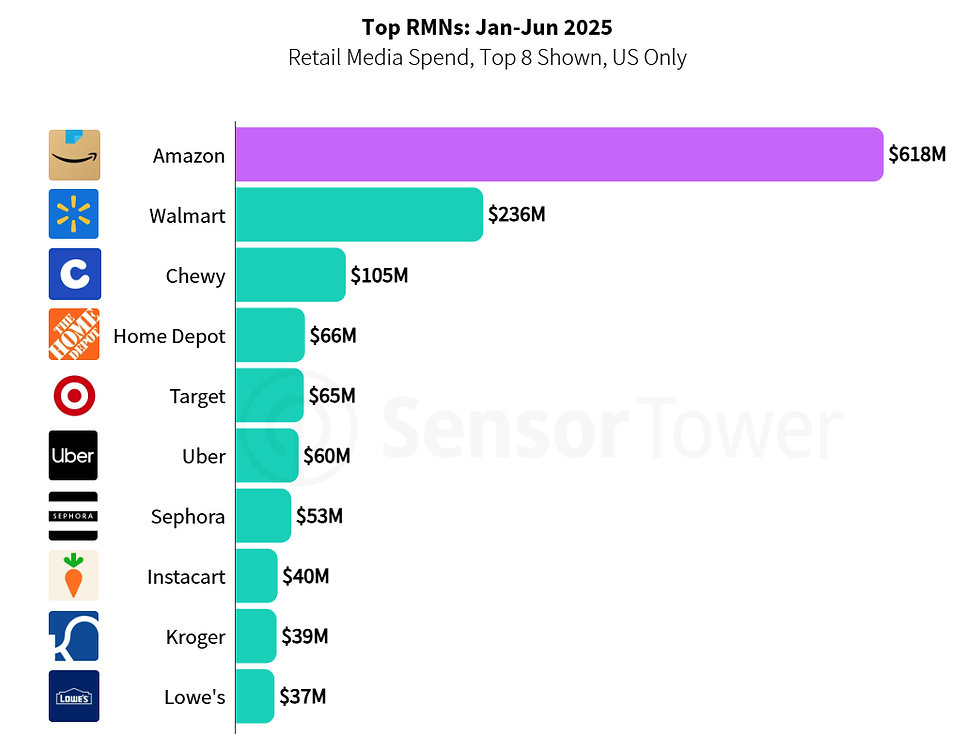

Amazon retail media: $618M H1, 3x Walmart

The big news this week was PCE data and Nvidia.

Nvidia delivered $41B in datacenter revenue. While it fell just shy of top-end expectations, the absolute scale confirms one thing: AI spending is alive and well.

We have been outspoken on this. The heavy lifting is happening now with NVIDIA, power providers, and data centers, the “picks and shovels” of AI. But the next phase is getting interesting: app building.

This is where the value is. It has to work.

The most important piece of this is tool calling. Connecting orchestration layers to siloed apps so AI can actually take action. Companies are working hard to build these connections, and we’re starting to see them.

Some jargon but MCPs (Model Context Protocols). Think of them as the connective tissue that lets AI call into business tools, APIs, and workflows in real time.

We just heard Box talk about strong demand after launching their MCP. That’s a sign of what’s coming.

On inflation, PCE came in right in line with expectations, and the chart below shows just how stable inflation has been over the past several years.

Some will argue that since inflation isn’t at 2%, the Fed has no reason to cut. But as we’ve said before, housing is the big driver. Inside PCE, housing is still showing +4.2% Y/Y.

But when we look at Apartment List data, the picture is the opposite.

Rents fell M/M last month for the first time since January.

Y/Y rent growth has been negative every month since June 2023.

Rental vacancies are now 7.1%, the highest in years.

This is why housing isn’t truly rising +4.2% Y/Y as PCE suggests.

We’re also seeing the metals basket roll over, and historically inflation data tends to follow that directionally.

At the aggregate level, concern over inflation is muted. Google search trends for “inflation” remain low compared to UMich sentiment readings.

Pulling it all together with real-time data, inflation sits at 2.15%, a bullseye for the Fed.

That’s inflation, but what about the other side of the mandate, jobs?

The labor market isn’t flashing red. Unemployment is steady and payrolls remain positive. But if you use ADP as a proxy for momentum, the picture softens.

ADP has been running below its 5-year rolling average, with the gap widening over the last 3–4 months. It’s not outright weakness (104k jobs added last month), but it is clear deceleration, enough to justify an “insurance” cut.

That’s what we’re gearing up for. Markets put the odds of a September cut at 87% and roughly 50/50 for October. If jobs weaken further, the Fed could be just in time, and deliver a 50bps cut.

The impact flows directly into anything tied to Fed funds, HELOCs, credit cards, SOFR-linked loans.

The implications are big.

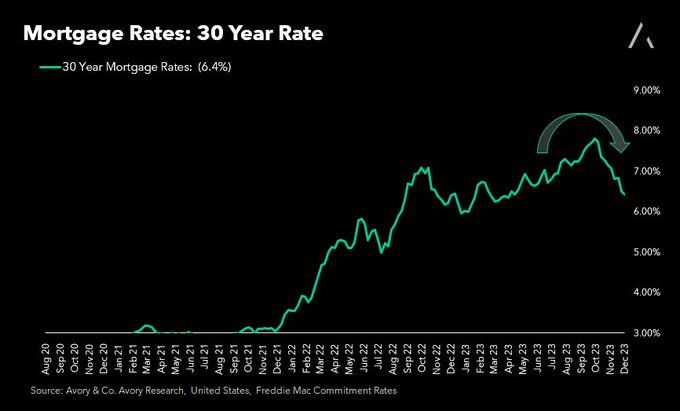

It also feeds into mortgage rates. The spread to the 10-year yield is still wide, but narrowing as mortgage rates have fallen 1.3% from their highs. It takes time for short-term cuts to work through, since prepayment risk props up the spread, but we’re already seeing lower short-term rates pressure longer-term rates down.

Lastly, Amazon’s massive ad share.

This chart shows retail media spend on Amazon, which matters in the goods inflation debate. We haven’t seen much goods inflation, possibly because the largest platforms selling goods also generate high-margin revenue outside of goods, giving them room to subsidize pricing pressures.

Amazon’s ad business is 3x the size of Walmart’s, and Walmart is 2x larger than its next competitor.

Overall a nice week. Have a great long weekend!

About Avory & Co.

Investing where the world is headed.

Avory specializes in high-conviction equity strategies, emphasizing Secular Growth and Transformation Stories driven by exceptional teams. Data guides decisions. We cater to high net worth investors, family offices, and institutional investors. Note: This information doesn't constitute a recommendation to buy or sell any mentioned securities. Avory is based in Miami, Florida with clients all across the globe.

Speak to us: Schedule a Brief Zoom Meeting

Send us an email: Team@avoryco.com

Want to invest? We are on most platforms.

Want More

🎥 Avory YouTube Channel

🎙️ Avory Podcast

Disclaimer: Not a recommendation to purchase or sell any securities mentioned. This is for educational purposes only.

Comments